News 2020

News Pictures 2020

")

Participation: Fudan University

![]()

Participation: Fudan University

09.01.2020. Georg Keilbar, PhD student of the IRTG 1792, was visiting Fudan University in Shanghai, China. He gave a talk on “Testing for Neglected Nonlinearity in the Conditional Quantile using Neural Networks” at the Quantitative Economics and Finance Seminar in the School of Economics.

Gender: Dr. A. Petukhina introduces academic junior staff

![]()

Gender

22.01.2020. Dr. Alla Petukhina, LvB Chair of Statistics almuni, introduces our youngest academic junior staff Alexander Maximilian Petukhin, who was born on the 01.11.2019, to our group.

All the best and only the happiest of moments!!

Participation: “Causal Inference and Machine Learning” Workshop St. Gallen

![]()

Participation: “Causal Inference and Machine Learning” Workshop

23.01.2020. Daniel Jacob, PhD student of the IRTG 1792, was visiting the “Causal Inference and Machine Learning” Workshop in St. Gallen. He gave a talk on “Does Tenure Make You Happy in Your Job? – A Machine Learning Approach”. During the two-day workshop keynotes were held by Uri Shalit (Technion - Israel Institute of Technology) and Stefan Wager (Stanford).

Haindorf Seminar 2020

![]()

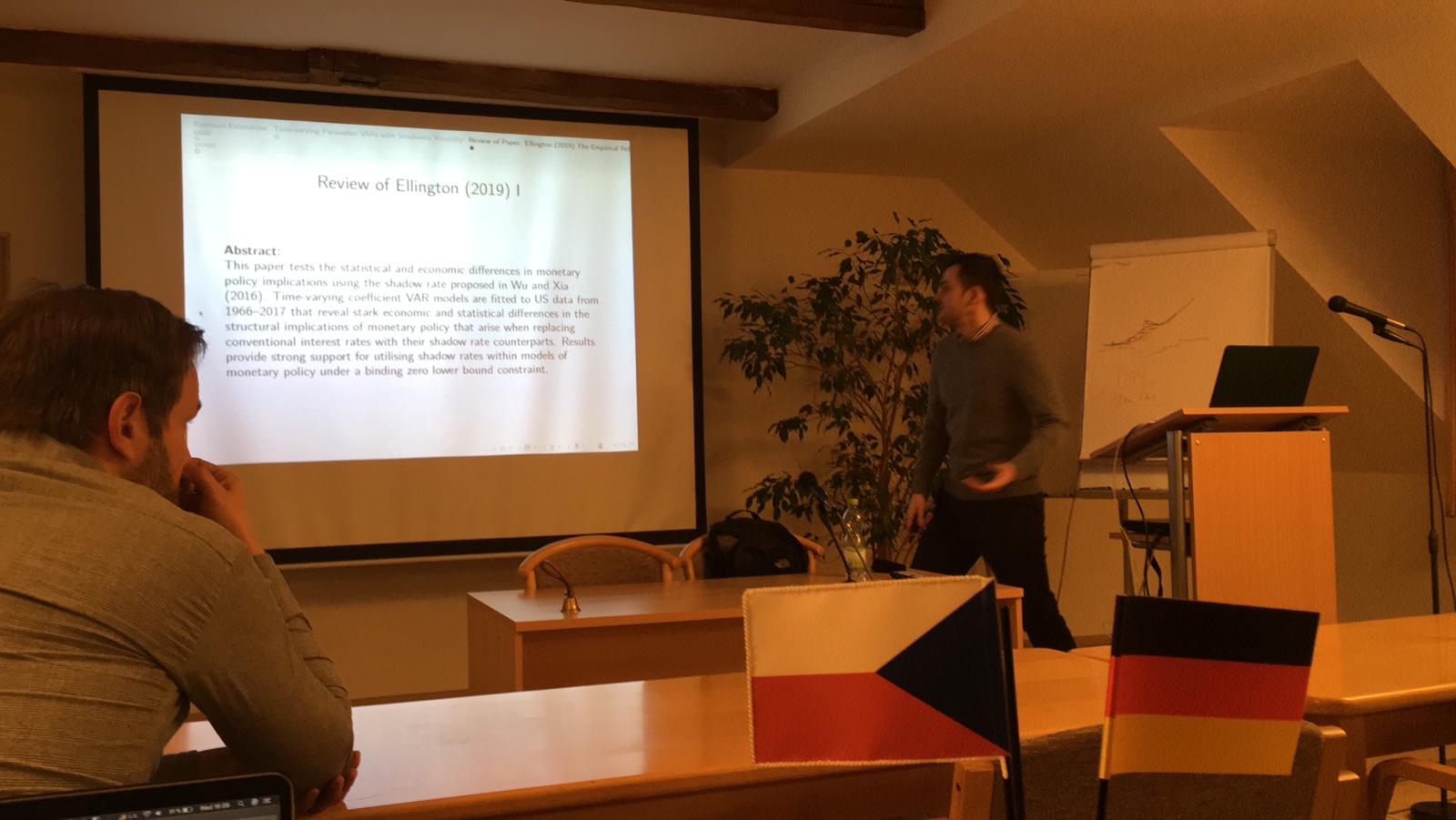

In cooperation with Charles University Prague, Haindorf Seminar 2020 took place from January 21 to 25 in Hejnice (CZ). During the seminar, PhD students of the IRTG 1792 and Charles University were given the chance to present their current research projects. Additionally to the talks and discussions, Andrew Vivian (Loughborough University/ UK) gave a short course on „Risk Management and Forecasting in Commodity Markets“ and Michael Ellington gave a short course on „Time-Varying Parameter Estimation in VAR models“. Besides the academic program, participants were given the opportunity to go skiing in the nearby Jizera Mountains and to visit the monastery of Hejnice, a historical pilgrimage destination. We thank all participants for their contributions and look forward to continuing the academic prosperous cooperation with Charles University Prague in the future.

There is more information about the participants as well as the talks on the seminar’s website.

Participation: Haindorf Seminar 2020

![]()

Participation: Haindorf Seminar 2020

28.01.2020. In cooperation with Charles University Prague, Haindorf Seminar 2020 took place from January 21 to 25 in Hejnice (CZ). During the seminar, PhD students of the IRTG 1792 and Charles University were given the chance to present their current research projects.

Additionally to the talks and discussions, Andrew Vivian (Loughborough University/ UK) gave a short course on „Risk Management and Forecasting in Commodity Markets“ and Michael Ellington gave a short course on „Time-Varying Parameter Estimation in VAR models“.

Besides the academic programme, participants were given the opportunity to go skiing in the nearby Jizera Mountains and to visit the monastery of Hejnice, a historical pilgrimage destination.

We thank all participants for their contributions and look forward to continue the academic prosperous cooperation with Charles University Prague in the future.

There is more information about the participants as well as the talks on the seminar’s website.

Participation: SFM I Trip to Frankfurt 2020

Participation: SFM I Trip to Frankfurt 2020

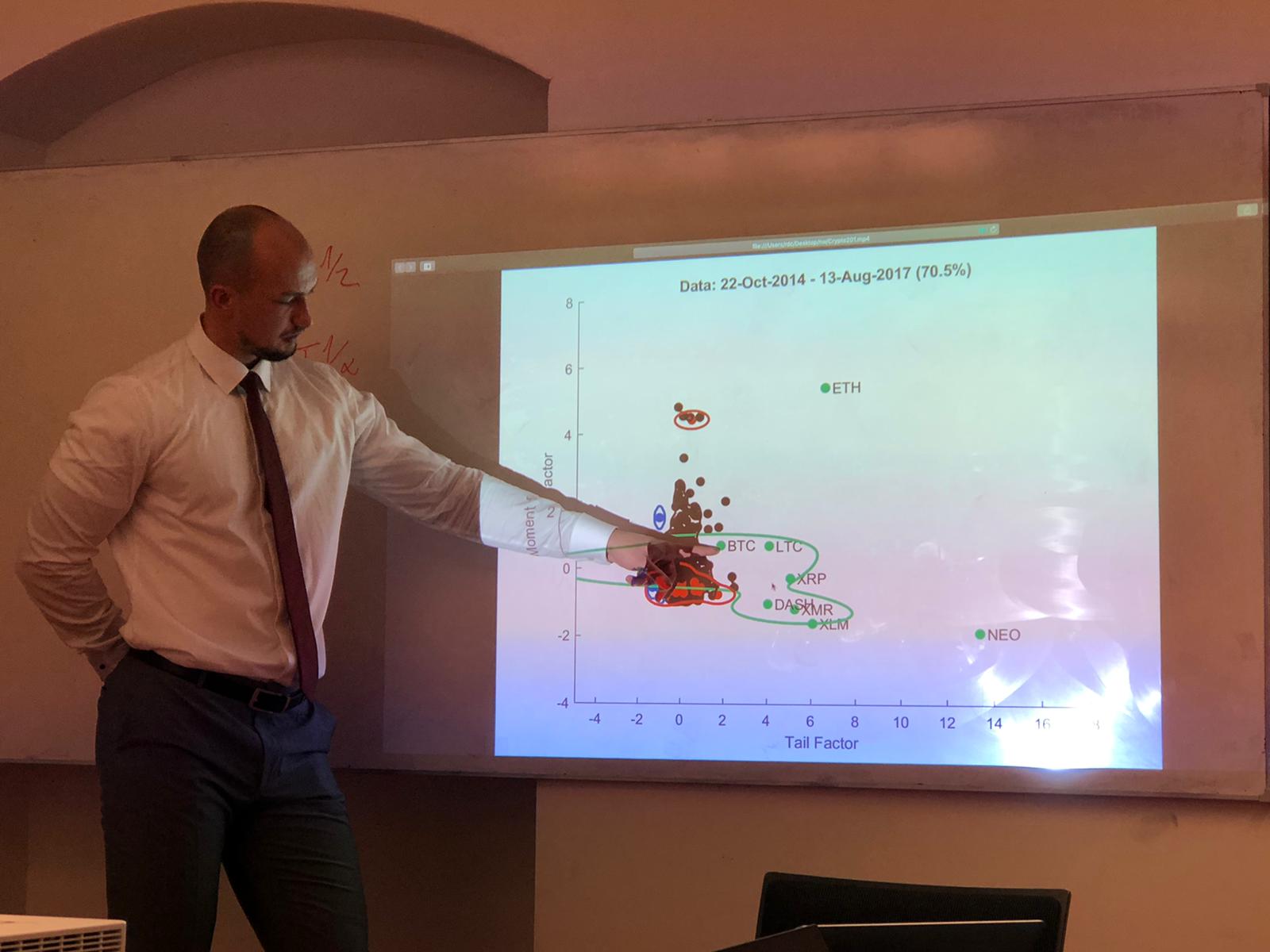

20.01.2020. Traditionally, the Statistics of Financial Market I exam takes place during a conclusive educational trip to Frankfurt. Besides the academic program, the students have the possibility to observe how quantitative research and trading departments work in large well-known financial institutions.

This year, two visits were planned: one in the European Central Bank (ECB) and the other in Deutsche Bank AG (DB).

In the ECB main building, the Statistics Department hosted the participants for two tailored lectures on the crypto-asset phenomenon, its risks and measurement issues. The visit was particularly fruitful as one of the speakers, Urszula Kochanska, will be part of the Blockchain Research Center Workshop 2020 organised by the IRTG 1792 in April.

In DB, Christian Schön welcomed the visitors in the Fixed Income trading floor, introducing them to the daily routine of the bank. During the afternoon, Dr. Marius Ascheberg showed the applicability of quantitative skillsets, while Nico Weinert gave an introduction to the Electronic FX trading. To complete the guided tour, Dr. Nicolas David illustrated the mathematical foundation of exotic interest rates derivatives.

We thank Prof. Dr. Wolfgang K. Härdle and the PhD candidate Junjie Hu for having offered this nice opportunity to the students and we are looking forward to the start of Statistics of Financial Market II.

Staff: Natalie Packham appointed Associate Editor for Digital Finance

Participation: Natalie Packham appointed

Associate Editor for Digital Finance

05.02.2020. Natalie Packham, Professor of Mathematics and Statistics at Berlin School of Economics and Law and Associated Researcher at the IRTG1792, and Uwe Wystup, Founder and Managing Direction of MathFinance AG, were appointed Associate Editors of the journal "Digital Finance - Smart Data Analytics, Investment Innovation, and Financial Technology”. They are also Guest Editors of a Special Issue of Digital Finance on Artificial Intelligence, Machine Learning and Platform Innovation in Quantitative Finance to be published in connection with the upcoming MathFinance conference later this year. Welcome on board!

Gender: Marie-Skłodowska-Curie Individual Fellowship

Participation: Marie-Skłodowska-Curie Individual Fellowship

Dr. Rui REN together with Prof. Dr. Weining WANG, applied to the EU Framework Programme for Research and Innovation entitled "Horizon 2020".

They received the Marie-Skłodowska-Curie Individual Fellowship with a amount of 174 806.40 EUR. The type of action is Standard European Fellowship.

The project title is "Quantitative Financial Risk Network Analysis with Sentiment and Herd Behaviour Measures", which is expected to be of 24 months starting within 12 months after the signature of Grant Agreement.

Dr. Rui REN will conduct joint research with Prof. Dr. Weining WANG on tail event driven sentiment network, quantifying investor sentiment, calibrating the option pricing model and detecting herd behaviour in the financial market. It potentially contributes to inclusive, innovative and reflective societies by supporting financial decision-making processes and managing risks for investors and institutions.

Participation: Finanstilsynet, Financial Supervisory Authority (Denmark)

Participation: Finanstilsynet

06.-07.02.2020. Wolfgang Karl Härdle, speaker of the IRTG 1792, Cathy YH Chen, Mercator Fellow of the IRTG 1792, and Raphael C.G. Reule, MD of the IRTG 1792, visited the Danish Financial Supervisory Authority (Finanstilsynet) at Copenhagen, which is the financial regulatory authority of the Danish government responsible for the regulation of financial markets in Denmark.

During this Horizon 2020 SupTech Event on "AI, Market Risk and Robo Advisory" they gave talks on "Data Science & Digital Society (DS2)", "Financial Risk Meter (FRM)", "Smart Contracts, and the pursuit of an interdisciplinary technical cure-all", and hosted a coding session.

Dissertation: N. Wesselhöfft completes PhD

![]()

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

.jpeg){kind=link}

{kind=link}

{kind=link}

Dissertation: Niels Wesselhöfft completes PhD

14.02.2020. Niels Wesselhöfft defended his PhD dissertation on "Self Similarity".

Congratulations!

Publication: "Adaptive weights clustering of research papers"

![]()

Publication

20.02.2020. Larisa Adamyan, Kirill Efimov, Cathy Y. Chen and Prof. Wolfgang Härdle's paper entitled "Adaptive weights clustering of research papers" has been accepted for publication in Digital Finance.

The abstract of the paper is as follows:

The JEL classification system is a standard way of assigning key topics to economic articles to make them more easily retrievable in the bulk of nowadays massive literature. Usually the JEL (Journal of Economic Literature) is picked by the author(s) bearing the risk of suboptimal assignment. Using the database of the Collaborative Research Center from Humboldt-Universität zu Berlin we employ a new adaptive clustering technique to identify interpretable JEL (sub)clusters. The proposed Adaptive Weights Clustering (AWC) is available on http://www.quantlet.de/ and is based on the idea of locally weighting each point (document, abstract) in terms of cluster membership. Comparison with 𝑘-means or CLUTO reveals excellent performance of AWC.

Congratulations!

Participation: Bundesbank Horizon 2020 SupTech Event

Participation: Bundesbank Horizon 2020 SupTech Event

10.-11.02.2020. Wolfgang Karl Härdle, speaker of the IRTG 1792, Stefan Lessmann, Principal Investigator of the IRTG 1792, and Rui REN, Postdoc of Fintech Horizon 2020 Project, attended a workshop named “AI, Market Risk and Robo Advisory” at the Deutsche Bundesbank at Frankfurt, which is co-hosted by the Fintech Horizon 2020 Project and the Deutsche Bundesbank.

During this Horizon 2020 SupTech Event, they gave talks on “Financial Risk Meter (FRM)” , “eXplainable AI (XAI) in Regulated Financial Services”, "Interpretable Machine Learning", and “Deep Learning Glossary in Layman Language”, “Network analysis” and “AI Use Cases”.

Publication: "Pricing Cryptocurrency Options"

![]()

Publication

09.03.2020. Ai Jun Hou's, Weining Wang's, Cathy YH Chen's, and Prof. Wolfgang Härdle's paper entitled "Pricing Cryptocurrency Options" has been accepted for publication in Journal of Financial Econometrics.

Congratulations!

Participation: Charles University, Prague

![]()

Participation

11.03.2020. Wolfgang Karl Härdle, speaker of the IRTG 1792, gave a talk on "SONIC: Social Network with Influencers and Communities" at the Charles University, Prague.

The abstract of his talk is given below:

Abstract

The integration of social media characteristics into an econometric framework requires modeling a high dimensional dynamic network with dimensions of parameter Θ typically much larger than the number of observations. To cope with this problem, we introduce a new structural mode SONIC which assumes that (1) a few influencers drive the network dynamics; (2) the community structure of the network is characterized as the homogeneity of response to the specific infuencer, implying their underlying similarity. An estimation procedure is proposed based on a greedy algorithm and LASSO regularization. Through theoretical study and simulations, we show that the matrix parameter can be estimated even when the observed time interval is smaller than the size of the network . Using a novel dataset retrieved from a leading social media platform StockTwits and quantifying their opinions via StockTwits and quantifying their opinions via natural natural language processing, we model the opinions network language processing, we model the opinions network dynamics among a select group of users and further among a select group of users and further detect the latent communities. With a sparsity With a sparsity regularization, we can identify important nodes in the regularization, we can identify important nodes in the network.

SitRep: COVID-19

![]()

Situation Report

13.03.2020. With the Coronavirus situation changing every day, we thought you may appreciate an update from us on how we aim to provide you with uninterrupted research over the coming days and weeks.

As it stands, all of the team here at the IRTG 1792 are fighting fit and healthy and it’s business as usual.

We are closely monitoring developments though, and we are taking extra measures to ensure we stay as healthy as possible and continue to fulfill our duties.

")

Enclosed you find the guidelines of the HU President regarding the immediate measures to prevent the spread of the coronavirus SARS-CoV-2, which were introduced on March 11th 2020. We ask you to observe and comply with the implemented measures and the information given below. Please forward the e-mail/information immediately to the staff in your departments.

Participation: Rheinische Friedrich-Wilhelms-Universität Bonn (University of Bonn)

![]()

Participation

26.05.2020. Rui REN, Anna Shchekina, Vanessa Guarino, and Michael Althof gave a talk on "FRM financialriskmeter for Cryptos", as well did Wolfgang K. Härdle present "Dei ex machinis, the attractiveness of p-hacking".

Publication: "TERES: Tail Event Risk Expectile based Shortfall"

![]()

Publication

12.06.2020. Philipp Gschöpf's, Andrija Mihoci's, and Wolfgang Härdle's paper entitled "TERES: Tail Event Risk Expectile based Shortfall" has been accepted for publication in Quantitative Finance.

Congratulations!

Event: IRTG 1792 Summer Camp 2020

![]()

Event

The annual IRTG 1792 Summer Camp took place at Buckow (Märkische Schweiz) from the 14.07.2020 - 17.07.2020.

Many thanks to all participants and staff, who worked as a team and made this event another successful one for the IRTG 1792. Special thanks to our industrial partners that have joined us, some of who need to remain unnamed, especially from Bitwala and dyos.

We are very glad to have found such a inspiring sanctuary, the Strandhotel Vierjahreszeiten Buckow, with such incredible positive and proactive staff!

")

SSRN Top Ten's: Rise of the Machines? Intraday High-Frequency Trading Patterns of Cryptocurrencies.

![]()

SSRN Top Ten Lists

Professor Wolfgang K. Härdle's, Speaker of the IRTG 1792, Dr. Alla Petukhina's, and Raphael C.G. Reule's, MD of the IRTG 1792, paper "Rise of the Machines? Intraday High-Frequency Trading Patterns of Cryptocurrencies", was recently listed on SSRN's Top Ten download lists for:

31.07.2020: Other Information Systems & eBusiness eJournal Top Ten.

01.08.2020: PSN: Exchange Rates & Currency (International) (Topic) Top Ten.

03.08.2020: International Political Economy: Monetary Relations eJournal Top Ten.

09.08.2020: Capital Markets: Market Microstructure eJournal Top Ten.

We featured this research outlet previously as IRTG 1792 DP 2019-020 here.